What is the bond market telling us about inflation?

There are few metrics that have a larger impact on a financial plan than the inflation assumptions. While we always know that projections are just that, our field is one of uncertainty. And putting together a reasonable estimate of how your costs are likely to change in the future is high on the list of critical inputs. Given the rise of inflation talk in the media, we wanted to take a brief moment to talk about what the bond market is telling us about inflation assumptions.

Disruptions in supply chains and labor shortages in certain markets have had a cascading effect on the cost of many consumer goods recently. And we also tend to look at housing costs as an indicator. By both of those metrics, we should be worried. The low supply of housing meeting rampant demand has led to steep increases in the value of homes in many markets around the country.

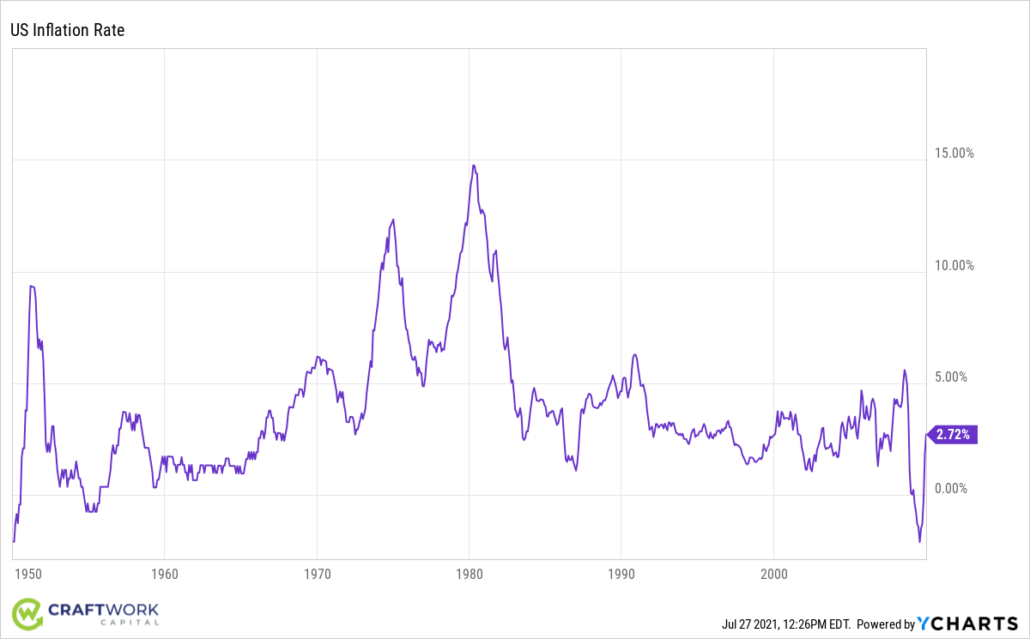

Historical inflation in the US has typically neared 4%, but certainly hasn’t remained constant. Looking at a 60 year period from 1950 to 2010, we can see that it has been quite volatile.

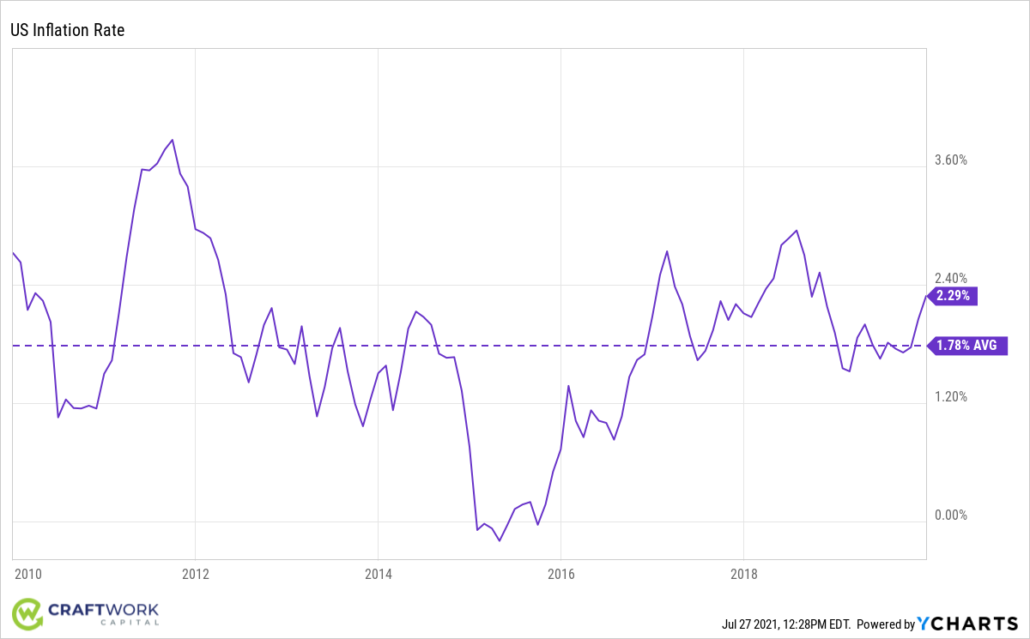

But in the last decade, we’ve had a very mild inflationary environment averaging less than 2%.

10 Year Treasury/TIPS Breakeven Rate

Looking at historical inflation gives us a good sense of where we have been, but says very little about what is coming. There is no shortage of economists and pundits that are discussing estimates for inflation. Some of these come from advanced modeling, and some are quite frankly just guesswork. While we don’t ignore those predictions, we prefer to look to the bond market for an indicator – the 10 Year Treasury Inflation Protected Security (TIPS) vs Treasury spread.

TIPS are government bonds that have inflation protection baked into them for the investor. As inflation rises, the amount the investor will receive from the bond rises with it. A regular Treasury bond does not have the same type of protection. As a result, an investor would typically be willing to accept a lower yield for the TIPS investment because they are not as concerned about inflation eroding their purchasing power. In a Treasury, the investor must require a high enough yield at the outset to handle inflation erosion.

Since a 10 year TIPS bond and a 10 year Treasury are both backed by the full faith and credit of the US government, we assume they have the same level of risk. And so the spread between the TIPS and Treasury yields becomes a surrogate for telling us how much inflation is expected.

Unlike the predictions that economists make, we like this indicator a lot because there is actual money behind it. Predictions and projections are cheap, and there is typically no cost of being wrong. The bond market is telling us where people are actually pricing this risk with real capital behind it.

So, what does it say?

While there has certainly been a spike in demand across the economy and rising prices as a result… The bond market is telling us that forward looking inflation is not as dire as some are predicting.

This data doesn’t mean that we as planners should be complacent. In fact, in the plans we do we don’t even use the same inflation rate for all spending items. We assume that certain costs like healthcare and college tuition rates will rise faster than other costs, so we assign them higher inflation estimates. We can’t be asleep at the wheel.

Keep Your Eye On What Matters

Up to this point, we’ve only talked about the inflation side of the equation. The thing you as an investor can and should be doing to combat this is growing purchasing power. After all, that’s why we invest, right?

The real return in your portfolio is the amount that your investments grow above inflation. This is the critical number.

If inflation stays low at 2% over the next 20 years and you earn 6% on your investments, you’ll be growing your purchasing power in real terms by 4% annually. Similarly if your investments were returning 12% per year, but inflation ticks up to 8% – you’ll effectively have the same situation. Your portfolio will be much larger in dollar terms, but from a purchasing power perspective it’s effectively the same.

In the planning work we do, we want to make sure we’re using fairly modest real return estimates so that even if we get inflation wrong, we can set our clients up to have the best possible chance to protect and grow their real purchasing power.

Book an Appointment Today, so we can help you stress test your plans for inflation and more!