So much of today’s commonly recited advice gets boiled down into bite sized pieces to make sure it’s easy to retain and remember. But in the search of these simple snippets, you may be doing yourself a deep disservice. Today we unpack five of the most common myths about retirement that are worth reconsidering.

- You must pay off your mortgage prior to retirement

- Convert to an income or dividend focused portfolio

- Getting older means you need more bonds/less risk

- Always wait as long as you can to max out Social Security

- You should expect to spend less in retirement

Myth 1: You must pay off your mortgage prior to retirement

Investors often set a goal of having a paid off home heading into retirement. At first glance this makes sense. Not having a monthly payment means a lower burn rate, and that you can get by on less income. But that’s not the only factor that matters. Thinking about your personal balance sheet holistically, storing large amounts of equity in your home isn’t always practical. We commonly joke that your home may be your largest asset, but try to go buy milk with a paid off home. It is an inherently illiquid asset.

This effect compounds another issue we commonly see, which is a lack of taxable savings. Many investors get to retirement and might have their entire nest egg wrapped up in 401(k) or IRA assets that they have been diligently saving into for years. If you have been directing all of your excess cash flow toward paying down the mortgage, it makes sense that perhaps you haven’t been investing as much, or at all, in a simple taxable brokerage account.

Foregoing taxable savings and investments can be a big mistake, especially if early retirement is a goal. Keep in mind that you cannot take normal distributions from retirement accounts until age 59 ½. There are a few ways to access that money without penalty, but it’s far easier if you simply have access to unrestricted assets.

Let’s imagine two families that each have a net worth of $500,000 as they head into retirement. We’ll call them the Montagues and the Capulets. The Montagues own a home that is worth $500,000. They worked hard to pay it off and now they can live debt free. The Capulets also have a $500,000 home they recently bought for retirement. They put $100,000 down, and have another $400,000 in liquid investments and cash. At 3.5% interest, their 30 year mortgage payment is $1,797 per month.

Both families have the same net worth, but who is in better shape? We would argue that the Capulets are in a much more flexible position, if not outright better prepared. They have liquidity. They could simply pay off the entire mortgage today if they choose to, but they could also live on the accumulated cash and investments. They can afford to take a trip. They can produce potentially higher returns than the equity in the home might deliver. Consider that U.S. home prices have appreciated by only 3.4% annually over the last 20 years[1], is your home really where you want all of your equity?

Now, let’s not get carried away here. Is a paid off home truly a bad thing? Of course not. If you’ve saved diligently and have both taxable savings and a paid off home, you may be in great shape. However, every dollar on your balance sheet needs a purpose. We propose being deliberate about how our clients treat each of those dollars. Keep in mind that a paid off home can be a comforting thought, but may not actually lead to the lifestyle you want to create.

Myth 2: Switch Your Portfolio to Dividend Payers

Those nearing retirement often ask how to transition to a more income focused portfolio that can provide a steady stream of dividends to support regular cash flow needs. In the past, this has been a successful strategy to collect income from a portfolio without ever spending down principal. However, there are multiple reasons that we don’t believe it’s necessary to convert a portfolio of high quality stocks you love all to dividend payers as you approach retirement.

Let’s start with the problem of yield.

Take a look at a chart of the S&P 500’s yield historically[2]:

The average (mean) yield of the S&P 500 has been 4.31%. That means a portfolio of ~$1.16 million would produce annual income of $50,000.

Currently, the S&P 500 yield sits at a paltry 1.63%. That means the same $50,000 of income would require $3,067,485, more than 2.5X as much initial capital. If you’ve saved enough to live on a 1.63% yield, you’ve done a great job. But most investors don’t want to save 2.5X more money simply to live on yield.

But what about higher yielding companies? There are companies today inside the S&P 500 that pay really impressive yields. In fact, a portfolio of the top ten S&P 500 dividend yielding companies currently produces more than 8% in annual income[3]!

While you might salivate at the thought of a carefree 8%+ of cash coming in, that same illustrated portfolio would have had returns of -5.25% per year over the last 5 years, versus the S&P 500’s 11.71% annual returns.

Put differently, if you had invested $1,000,000 into those ten companies five years ago and not taken a dime out, today you’d have $763,653. Whereas if you had simply invested in the S&P 500 with the same $1,000,000, today you’d have $1,739,643. You’d be almost a million dollars worse off for having chased yield.

Instead of reaching for yield and potentially falling into value traps, we propose a total return oriented approach. We can continue to invest in high quality businesses whether they pay dividends or not as long as you have enough cushion to ride out poor market performance.

We prefer to “Carve Out” 3-5 years worth of your expected capital needs, at a minimum. Those assets should be in very low risk instruments like cash and conservative high-quality bonds. That means we have a relatively safe pool of money to draw from during periods that stocks are not performing. But we aren’t limiting ourselves to an investing universe of high dividend stocks looking for yields that may not be as good as they seem on the surface.

Myth 3: More Age = Less Risk?

There used to be an adage in investing to come up with your ideal bond allocation:

Percentage In Bonds = 100 – Your Current Age

So if you’re a twenty year old investor, 80% of your money is in stocks. By the time you’re sixty, you’re down to just 40%. Very simple. It seems to make sense at first blush. As we age, we might have less recovery time from bad markets. Or perhaps we simply don’t need to grow the money as much, inflation is less of a concern. We continue to hear age used as a proxy for how much risk should be in a portfolio. Investors will ask, “How much should I have in stocks at my age?” Using age as a proxy for risk tolerance is sloppy and can lead to drastically worse performance over your investing lifetime.

We look at the risk in a portfolio according to two vectors:

- The capacity to take risk

- The desire and willingness to take risk

Let’s address the first: capacity.

Your capacity to take risk is a function of your time horizon, expected withdrawals, and flexibility.

Time horizon is the simplest of these. When do you expect to start drawing from your investments? In any single year, you have about a 75% chance of the market being up. Or, we should think of it as a 25% chance of the market being down. To avoid that, we want to be moving out of stock assets in the 3-5 year window preceding the expected spend.

The amount of the expected withdrawal need helps us understand how much of the money will be needed. If I’m only expecting to need 3% of my savings per year, I have the capacity to be considerably more aggressive than someone who needs 5% of their savings per year. So we must look at what the potential spend down really looks like.

Flexibility might be the hardest to quantify, but this is where some of the real financial planning questions come into play. Let’s look at examples.

If you are planning for college tuition, this is likely a fairly inflexible goal. Most students will enroll in college in the fall after their senior year of high school. The time frame you are likely to write a tuition check for this money can be predicted within a few weeks in either direction. Barring a situation where a student takes a gap year off, or chooses to defer enrollment, this is a fairly inflexible goal. We can look at this similar to an industry that might have a mandatory retirement date making work beyond anticipated retirement less likely.

Other industries have lots of flexibility. If the market is poor in the year you hoped to retire, maybe you simply work another 12-18 months and wait for a recovery.

How open you feel personally about that flexibility and those choices all impacts capacity for risk. Once we understand the capacity for risk, we can look at your investing preferences. Do the ups and downs of the market make you queasy? Or are you a gun-slinger of an investor that wants the high flyers and next hot thing in your portfolio? Most investors quite frankly have a bit of both mentalities at the same time. Investors tend to adjust their tolerance or willingness for risk based on how they feel. I’ve observed big swings from desiring a fully stock invested portfolio to a very conservative one based on just a few weeks of market behavior.

Our hope is that we can be as honest as possible with ourselves so we don’t end up making wild adjustments. But having a strong handle on capital needs and risk capacity will make staying the course much easier in the face of market turmoil. Taking a holistic look at your portfolio might ultimately mean that we find you aren’t likely to spend all of your resources during your lifetime. Or perhaps you have a goal of leaving a legacy to children, grandkids, or charitable endeavors. If that’s the case, perhaps your portfolio could be significantly more aggressive in your 70s or 80s than you needed to be making the approach to retirement at 60.

We want to do our best to avoid sloppy shortcuts that could end up costing your legacy interests hundreds of thousands, or even millions in potential growth.

Myth 4: Always Delay Social Security to Increase Benefits

For many retirees, Social Security represents a major building block of their retirement strategy. The decision on when and how to claim can affect hundreds of thousands of dollars of potential retirement income over the course of a lifetime. Mistakes can be costly as well. But so much of the advice that is written about this topic comes from a single lens – get the most from the government!

At first glance, that might be exactly what you want. And perhaps a maximization strategy is right for you. But it’s critical to make your decision around Social Security in the context of your overall financial situation, not simply trying to squeeze the most out of Uncle Sam.

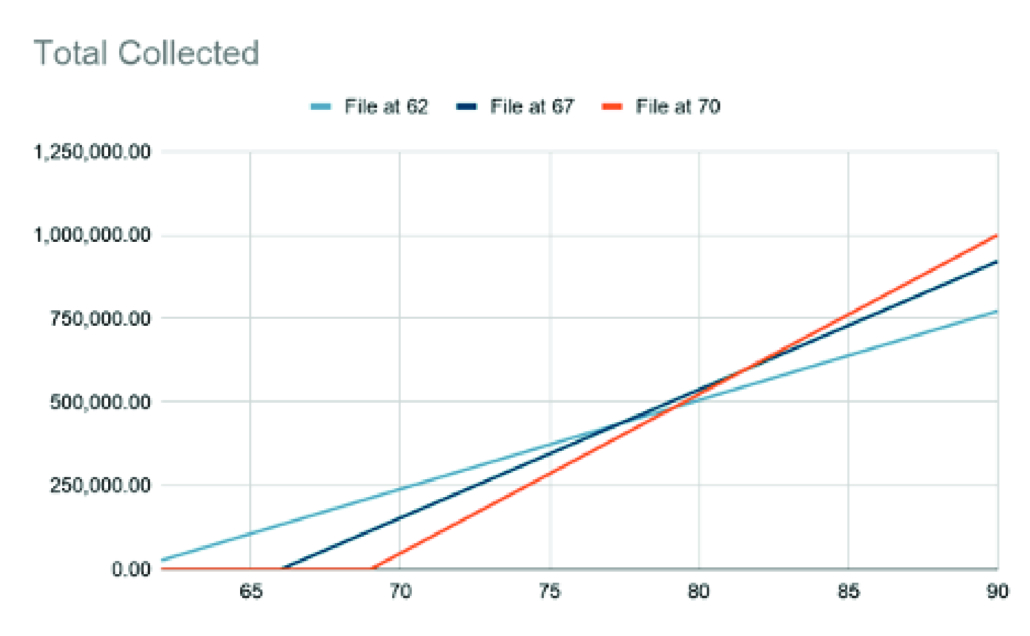

You have the ability to claim your Social Security from age 62 all the way up to 70. 62 is considered an early filing. And for each year beyond 62 that you wait, the amount you’ll receive monthly is increased.

If you wait until age 70 for the maximum increases, you typically have to live beyond age 80 to “break even” on the decision to wait. Which means you’ll collect about the same amount from 70-80 that you would have from 62-80. Beyond that age, you’ll be collecting clearly more in benefit.

Here’s what it looks like:

[4]

Given that longevity tends to be higher now than it has been in the past, if you are in good health, it makes sense that you can simply make a bet on your life expectancy and roll with it.

Unfortunately, that’s not all there is to it.

The flip side of the coin is understanding what you will live on in the meantime without claiming Social Security. For some, that means continuing to work. Or if you choose to retire before you’re ready to claim, your savings likely has to make up the difference.

Let’s take an example to the extreme.

Let’s assume your Age 70 Social Security payout was plenty to live on, not a worry in the world. But in order to make it to Age 70, you had to spend every dime of savings to be able to afford waiting. Is this worth it? From an income security standpoint, perhaps. From a legacy standpoint, perhaps not. If you are married, your benefit and your spouse’s will work together. Your partner may be eligible to benefit from a widow/widower benefit. But Social Security does not leave a legacy for children the way your assets do. So if you wait until 70 and then pass shortly after, you have collected very little, and spent all of your money trying to wait.

Even in this very simple hypothetical there are a number of considerations that would be critical to making a recommendation on whether to delay Social Security.

The goals you have for your portfolio, level of security, legacy… they all have an impact. Making a Social Security decision in a vacuum might get you the biggest payout from the government, but it might be at the expense of what you could have provided for your family.

Myth 5: You should expect to spend less in retirement than when working.

Another area where rules of thumb can be exceptionally dangerous to your long term planning is in your expected retirement spending. Online calculators commonly use a formula like 70-80% of what you make today. I believe they jump to this conclusion far too quickly, and you should be wary if you’ve been basing your plans on such a number.

Shortcuts are used here because most people planning for their retirement don’t actually have an accurate handle on their budgeting. Higher income individuals that have not felt budget pressure tend to have a casual relationship with their spending. And while I’m not advocating for a strict accounting, or even a reduced spend… understanding what it costs you to live is the most critical number in your retirement plan.

Having elaborate Excel projections and models of your investment assets is not helpful in the least if we start from a bad spend assumption. If you’re reading this and wondering who these people are that don’t know how much or what they spend their money on, you can jump past this exercise. But for the rest of us, I’d like to propose a math problem.

- Start with your income from the last year (calendar or simply the last 12 months)

- Subtract out the amount you paid in income and employment (FICA) taxes

- Subtract out your total savings for the year (401(k) contributions, and all saved funds)

- Subtract out any large one-time financial impacts that won’t repeat

- What is left is what you spent on your lifestyle in the last year.

Rather than starting with things like your fixed expenses and building up to a budget, we prefer to work backwards. Building up to a monthly budget tends to miss all sorts of less frequent costs that we simply bake into our budget and never think twice about. For example my car property taxes that are always due in October and I never think twice about for the rest of the year.

Now that you have a good handle on what a year of your life costs, you can make further modifications depending on where you are in life. If you’ve got kids at home, there are clear financial costs that are adding to your food, clothing, travel, activities, etc. that likely won’t continue into retirement.

You should also think about the things you want to add to your life as a retired person, and make sure you’re adding those back into your expected spend. If you currently take a single vacation per year, but plan to spend multiple weeks per year traveling the world once you’re no longer working, you need to be preparing for those increases.

We’ve found that many people don’t actually reduce their spend much from what it is during their working years. If we can help it most of us want to retire to a lifestyle that is equal to or better than what we currently have in the workforce. To assume that we’ll simply spend less through a short-cut formula is sloppy and ignores so much of what will determine if your retirement is a happy one or not.

We hope our dissection of common retirement myths has been helpful. But we believe the best way to truly understand if you are positioned well for retirement is to work personally with a fiduciary advisor that can help you model your situation and consider your exact circumstances.

Book a Consultation with a member of our team to see if our practice capabilities are a good fit for your retirement needs!

[1] https://am.jpmorgan.com/us/en/asset-management/gim/adv/insights/guide-to-the-markets/viewer

[2] https://www.multpl.com/s-p-500-dividend-yield as of 11/16/2020

[3] Top 10 dividend payers sourced from https://www.youngresearch.com/researchandanalysis/dividend-investing/the-highest-yielding-sp-500-stocks/, yield sourced by equal weight portfolio allocated to OKE, MO, XOM, IRM, KMI, LUMN, SPG, SLG, VLO, WMB via Morningstar.

[4]Chart created using sample estimated SSI payout values at age 62, 67 and 70. SSI data accessed on 11/16/2020. Applying no inflation to this estimated payout.